Asia-Pacific’s digital revolution is unfolding at pace. The region’s young, tech-savvy population, the bypassing of outdated legacy infrastructure found in Western markets, and concerted government support are combining to make APAC a frontrunner of digital adoption. Global investors are paying close attention to these unique fundamentals, pouring capital into data centers, telecom, fintech and AI. The result is a groundswell of dealmaking as companies race to secure their seat in the region’s digital-first future.

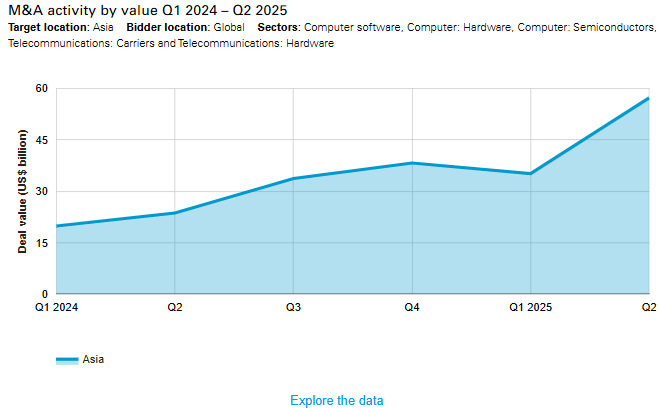

M&A transactions linked to APAC’s digital transformation have ballooned in value this year. By the end of H1 2025, total value stood at US$92.4 billion across 1,195 deals, making for a 113 percent year-on-year value gain, despite a 9 percent dip in volume. At the time of writing (September 10), this year’s value had reached US$111.7 billion, surpassing the total for the first three quarters of 2024 (US$77.2 billion) and setting the stage for one of the strongest years on record.

Scale deals

Topping the league table, Nippon Telegraph & Telephone announced plans to acquire the shares not already in its ownership in NTT Data, for US$16.4 billion. NTT Data is one of the world’s largest IT services providers, with a footprint spanning cloud migration, systems integration and digital consulting. By bringing the subsidiary fully in-house, NTT is betting on tighter integration between its telecom backbone and digital services arm, a move that positions it to compete more aggressively with global peers. The transaction speaks to rising corporate demand for consultative support as end-to-end digital transformation accelerates.

China, meanwhile, saw its largest-ever deal in the computing power industry: the US$16 billion merger of chipmaker Hygon Information Technology with its top shareholder Dawning Information Industry, a supercomputing and data center specialist. The tie-up creates a national champion in an increasingly strategic area for China’s digital economy. Computing power is a critical enabler of digital transformation as AI development and data demands intensify.

India has been another hotbed of activity. In March, the government increased its stake in Vodafone Idea, reinforcing the stability of one of the country’s largest telecom operators. With India’s digital economy rapidly expanding, from fintech adoption to AI services, robust telecom infrastructure is a prerequisite. By stepping in, the state signaled just how important connectivity is to sustaining the country’s digital transformation.

Further government-led support of India’s digital economy is evident in initiatives such as the Unified Payments Interface. Operated by the National Payments Corporation, the interface is a government-backed payments network that processes around 600 million transactions per day. Banks, payment aggregators and fintechs are using this infrastructure to offer credit, insurance, loans and other financial products, creating fertile ground for venture funding and M&A activity.

In July, France-based Schneider Electric announced a US$6.4 billion deal to take full control of its Indian subsidiary. The unit focuses on digital energy management and industrial automation—areas that are vital as India builds out smart factories, modernizes its grid and seeks more sustainable pathways to growth. For Schneider, the acquisition reflects confidence in India’s role as a digitized infrastructure hub and a recognition that the next stage of industrial growth will be digitally enabled.

Outside of these strategic megadeals, private capital is also actively targeting digital infrastructure. Stonepeak’s US$1.3 billion investment in pan-Asian data center operator Princeton Digital Group—which already counts Mubadala, Warburg Pincus and the Ontario Teachers’ Pension Plan among its major global investors—reflects rising demand for hyperscale capacity that can handle what are anticipated to be exponential AI workloads across the region. This follows on from Blackstone’s US$16 billion AirTrunk acquisition in Australia last year. The Japanese market is also recording considerable AI-related investment. In April, SoftBank Group announced that it was forming a joint venture with ChatGPT-creator OpenAI to develop enterprise AI solutions for businesses in Japan.

Fundamental drivers

Demand for computing power across APAC is accelerating at a pace that outstrips supply. CBRE forecasts that regional data center capacity will double by 2028, yet the market could still face a shortfall of 15-25 GW as AI workloads push existing facilities beyond their limits. Southeast Asia alone is expected to triple capacity by 2030, driven by a tenfold increase in AI-related demand. With power and land availability already acting as bottlenecks in key hubs like Singapore and Hong Kong, competition for modern, AI-ready infrastructure is intensifying, fueling higher valuations and sustained investor appetite.

In India, policymakers are responding to the same pressures with a raft of initiatives designed to expand digital infrastructure and accelerate adoption. The government’s National Broadband Mission 2.0, announced in January 2025, targets high-speed connectivity for hundreds of thousands of villages. Regulators are also stepping in, with the Reserve Bank of India piloting a sovereign cloud service for financial institutions, part of a wider push for data localization and cybersecurity. States are moving, too. In May, Central Indian state Chhattisgarh announced the creation of the country’s first AI-centric “special economic zone,” complete with high-density data centers tailored to machine-learning workloads. Collectively, these efforts are pulling capital into the infrastructure and platforms needed to sustain India’s rapid digital expansion, creating fertile ground for M&A in telecom, data centers and AI ecosystems.

China’s forthcoming 15th five-year plan is expected to reinforce the state’s techno-sovereignty agenda. While the plan is still in draft, early signals suggest that Beijing will prioritize strategic industries including AI, semiconductors, quantum computing, cloud and cybersecurity, treating them as pillars of economic growth and national security. The focus on “strategic endurance” signals the country’s determination to reduce reliance on foreign technology and insulate the digital economy from external shocks. This policy direction is already driving capital flows into domestic chipmakers, data center operators and AI developers, with more likely to come once the plan is announced next year.

In Southeast Asia, meanwhile, policy is directly shaping supply-side infrastructure growth. Singapore’s Digital Connectivity Blueprint, for example, launched in 2023, outlines strategic commitments for upgrading subsea cable capacity, next-generation data centers and frontier technologies like green software and quantum networks.

In Indonesia, the government is rapidly advancing digital infrastructure through both public investment and financial incentives. A national AI strategy, expected to launch imminently, aims to clarify infrastructure needs and attract foreign investment, especially in sectors such as health and agriculture, by clearly defining the requirements for data centers and other AI-linked digital infrastructure.

Risk vs reward

While governments across APAC are fully embracing digitalization, their rules diverge. China’s data localization laws, for example, require information to be stored onshore, while India introduced its own Digital Personal Data Protection Act in 2023, and Japan and South Korea maintain distinct cybersecurity frameworks.

For cross-border buyers, this patchwork increases integration costs and raises the risk of regulatory missteps. Add to that the broader geopolitical environment—US-China tech tensions, shifting tariff and trade policies, and hawkish export controls—and many deals face heightened execution risk.

Energy consumption is another bottleneck, as hyperscale data centers and AI clusters are voracious consumers of electricity. In Singapore, a moratorium on new data center construction was only lifted in 2022, and then only under strict efficiency requirements. Australia and Japan face similar pressures, with projects competing for scarce renewable power sources as governments push to decarbonize grids. For investors, the challenge is building new capacity that satisfies sustainability mandates while securing long-term energy supply.

The intensity of competition for assets, particularly data centers and AI-ready platforms, has also pushed valuations to record highs. Blackstone’s AirTrunk acquisition last year underscored how much investors are willing to pay for scarce infrastructure, which in some cases may be difficult to justify.

Blackstone paid 21x AirTrunk’s run-rate EBITDA, putting it broadly in line with, but on the high side of, multiples commanded by publicly traded peers like Equinix and Digital Realty. This ratio factored in future committed project revenues, but based on straight-line, forecasted 2024 earnings, the multiple could be as high as 87x EBITDA.

Opportunity knocks

These challenges aside, the momentum behind digital transformation shows little sign of abating. The structural factors underpinning the trend, including population growth, rising incomes, urbanization, government backing and technological necessity, are too powerful to ignore.

Dealmaking will, however, remain unevenly distributed. The largest economies of China, Japan and India will capture the bulk of digital M&A activity in the near term. Yet there is scope for dealmakers to look further afield. Emerging markets such as Vietnam, Indonesia, the Philippines and Malaysia are beginning to attract increasing attention as first-mover opportunities. These markets may lack scale today but could eventually deliver outsized returns for those prepared to take on more execution risk.

With demand rising, competition intensifying and technology embedding itself more deeply into society, digitalization will remain one of the defining features of dealmaking in the APAC region for years to come.

[View source.]

link